Subscribe to Our Weekly Newsletter

ISS is the most comprehensive source for self-storage news, feature stories, videos and more.

The CMBS (commercial mortgage-backed securities) bond market is back. After slowly returning to life in 2010, the capital markets appear to be in full recovery mode, with more than 20 active conduit lenders. Recent transactions provide evidence that this capital is readily flowing to and having an impact on the self-storage lending market.

May 12, 2011

Lending Is Back")

The CMBS (commercial mortgage-backed securities) bond market is back. After slowly returning to life in 2010, the capital markets appear to be in full recovery mode, with more than 20 active conduit lenders. Recent transactions provide evidence that this capital is readily flowing to and having an impact on the self-storage lending market.

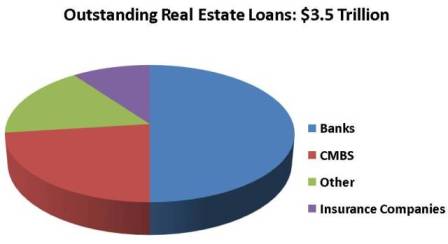

As a quick review, CMBS are bonds backed by commercial mortgages. A basic CMBS transaction structure starts with lenders who originate and aggregate pools of loans on commercial properties, and then sell the income stream from the mortgage payments to investors in the form of bonds. When the bonds are sold to the investor community, capital is returned to the lender, who is then able to redeploy it and make more loans. In this structure, capital flows efficiently between borrowers, lenders and investors; hence the name conduit is given to lenders who use this finance approach.

Through the first quarter of this year, CMBS issuance was at $8.7 billion. Most notably, Extra Space Storage Inc., the Salt Lake City-based real estate investment trust, received an $82 million first mortgage from Bank of America in January. The capitalthe companys first CMBS loan since February 2007was used to finance a portfolio of 16 facilities, according to chief financial officer Kent Christensen.

As the financial markets hit bottom in 2008, liquidity almost entirely dried up, and the CMBS market, for all intents and purposes, disappeared. As a result, self-storage operators, along with all other types of commercial real estate borrowers, were forced to use more traditional lenders such as local and regional banks. The net effect of this was less capital available at more stringent terms, including lower leverage, higher debt-service coverage ratios (DSCR), more conservative underwriting, and personal recourse.

More specifically, consider that during the glory days of 2007, CMBS lenders were originating non-recourse debt with a 10-year term and 30-year amortization, at 80 percent loan-to-value (LTV) and 1.20x DSCR. Often the underwriting included credit given to income based on projected future rental increases. In contrast, by the time the market hit rock bottom in 2008/2009, there were no CMBS lenders active in the market, and those lenders that were still originating loans on their balance sheets were doing so with extreme caution: 60 percent LTV, minimum 1.50x DSCR, with income underwritten to a strict trailing 12-month historical income and a look-back of two years or more to guarantee stability of the cash flow.

As a result, the self-storage lending market for many small and mid-sized operators ground to a halt, and even the largest operators were challenged to secure debt on their maturing loans. Those in need of loans (whether for construction, refinancing or acquisitions) were left in a precarious position, with properties worth an average of 20 percent to 30 percent less than they had been pre-crash.

To make matters worse, loans sized to 60 percent LTV down from 80 percent LTV forced borrowers to contribute a 20 percent larger stake in their facilities, difficult for many operators. A significant portion of commercial real estate properties, including self-storage, fell into delinquency, and borrowers were forced to agree to loan terms that some would consider egregious. The alternative was to lose their properties.

The emergence of CMBS as a capital source for commercial mortgage lending brought liquidity to commercial real estate that did not exist prior to 1990. As it re-emerges in 2011 and beyond, it should be welcomed with open arms by the banks, insurance companies and other market participants to help balance borrowers access to capital. Now, fully three years later, signs of life abound, and there is plenty of reason to be optimistic.

Steps Forward

With CMBS origination for 2011 estimated at $40 billion to $50 billion, up from $12.3 billion in 2010, its safe to say the CMBS market is back. At the Mortgage Bankers Associations annual conference in February, 27 lending institutions identified themselves as CMBS loan originators, a figure similar to the glory days of 2007.

With a larger supply of capital, CMBS lenders are actively seeking quality self-storage deals for the first time in almost three years. Generally speaking, these lenders are sizing loans at up to 70 percent LTV and 1.45x DSCR, with rates at 175-250 over the 10-year swap rate. At the swap rates existing at the time of this writing, this represents a bottom-line interest rate in the 5.50 percent to 6.25 percent range.

In general, CMBS lenders are only considering a smaller subset of self-storage facilities. Todays active CMBS programs have loan-size and other restrictions that do not heavily favor industry economics. For example, many lenders have implemented loan minimums ($5 million and up) that present a major obstacle for many self-storage owners and investors, essentially limiting potential to portfolios in larger markets and controlled by institutional-quality sponsors.

There is hope for smaller facilities and those outside urban cores; however, as these same lenders are starting to consider smaller loans (less than $5 million) in secondary and even tertiary markets. As the available capital continues to grow, simple supply and demand dictates that lenders will begin competing for more modestly sized loans.

Additionally, the liquidity that CMBS offers the market will take pressure off the system down the line, freeing up capital at the regional and local bank level. With CMBS lenders providing a much needed outlet for larger financing transactions, local and regional banks will once again be able to concentrate on a greater number of borrowers, such as self-storage owners with smaller loan needs.

Through the first quarter of 2011, CMBS issuance was $8.7 billion, on track to hit the projected issuance of $40 billion to $50 billion. As expected, these transactions have smaller dollar sizes and loan counts, with higher DSCRs and lower LTVs. And though 2011 projections are just a fraction of the peak levels that preceded the financial crisis, they do indicate positive movement; and the recent CMBS activity represents a significant share of overall lending in today's more cautious environment.

The Role of Self-Storage in the CMBS Market

The proliferation of CMBS prior to 2008 made it a desirable financing option. With five- to 10-year fixed-rate loan terms, low interest rates and high LTV financing of 75 percent to 80 percent, without a requirement for personal guarantees, it quickly became the preferred option for self-storage operators.

Self-storage has outperformed all other property types in terms of CMBS loan-delinquency rates throughout the recession, a fact that will surely resonate with lenders and investors as financing markets improve during the next few years. Additionally, conduits will be attracted by the self-storage asset class, as a more diversified set of properties in the issuance pool is appealing to bond investors looking to minimize asset class risk.

Its expected that CMBS underwriting for any new deals will be more conservative than it has been historically. However, when compared to terms self-storage operators receive from regional and local banks, CMBS is often the better option, if available. Though the process to finalize a CMBS loan includes arduous loan-documentation reviews, severe early pre-payment penalties and possible loan-size requirements, the positives (lower rates, more amenable terms and non-recourse mortgages) far outweigh the negatives. For self-storage operators seeking financing, these factors point to a healthier outlook for 2011 and beyond.

Based in Chicago, Shawn Hill is a principal at The BSC Group, where he provides mortgage brokerage, financial consulting, and loan-workout solutions to self-storage real estate owners nationwide. He can be reached at 312.207.8237; e-mail [email protected] ; visit www.thebscgroup.com.

You May Also Like